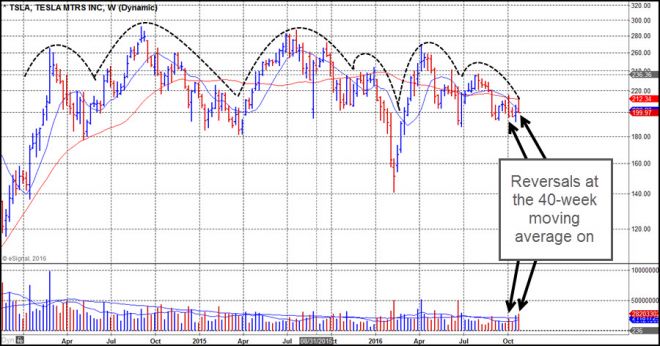

Tesla Motors (TSLA) announced earnings on Wednesday of this past week, sending the stock gapping up to its 200-day/40-week moving averages. The stock then reversed on heavy volume and is now just below the $200 price level and its 50-day/10-week moving averages.

On the weekly chart, below, we can see that the stock has been forming a large "mountain range" type of topping formation that has the look of a very busy, complex, and extended head and shoulders formation over the past three years, roughly.

With the stock sitting about 2.5% below its 50-day (on the daily chart) moving average and about 1% below its 10-week (on the weekly chart) moving average, it is in an actionable short-sale position using either the 50-day/10-week lines at 205.20/202.23 as guides for tight upside stops. Alternatively, one could give this more room by using the 200-day/40-week moving averages at 212.34/212.81 as guides for a slightly wider upside stop.

TSLA long ago lost its upside price momentum, and since early 2014 has merely moved back and forth within a wide, "mountainous" range. As the reality of the true profitability of its business slowly emerges, it is likely to eventually be valued more in line with any other auto manufacturer. In fact, if we look at current U.S. auto sales reported on October 3rd, we can see that TSLA's vehicles don't even rank in the top 20.

TSLA delivered 24,821 cars in the third quarter of 2016. At that rate, even by the end of the year, it won't even surpass the year-to-date sales of the Subaru Outback, the last-place finisher in the list above. Much was made of TSLA reporting "free cash flow" of $176 million, but this was achieved by accounting sleight of hand, whereby the company allowed accounts payable to increased from $1.1 billion last quarter to $2.3 billion in the most recent reported quarter. So the much ballyhooed increase in TSLA's Q3 free cash flow was achieved by the simple act of not paying its bills!

If TSLA is going to somehow grow into its valuation and avoid being lumped in with a stock industry sector that typically sees established names like F or GM selling at 5-6 times forward earnings estimates, it has its work cut out for it. So far, the price/volume action of the stock appears to argue against this. Thursday's price reaction and reversal showed that investors weren't snowed by the phony free cash flow numbers. We would not be surprised to see the stock eventually test the 141.05 low of February over time.

Of course, longer term, TSLA is working on a number of potentially ground breaking technologies which, if realized, could make a material difference to its bottom line. But that is for the future which does not exist. What matters is price/volume action in the present. And at present, the stock is telegraphing troublesome signs.