General

We are potentially at an inflection point in terms of the sawtooth, back-and-forth, trendless market action that has characterized the rally off the early June lows, given that the last three days of extreme tightness in the major indices is constructive. This attempt to consolidate prior gains is distinctly different from prior peaks in the summer rally where the market indexes quickly reversed course. Economic news has not been debilitating to the market as recent jobs and labor reports, starting with the Bureau of Labor statistics number on Friday August 3 have been better than expected. This past week, following the BLS report, further strength in the jobs market was evident with job postings at a four-year high and jobless benefit claims slowing. And while European Central Bank Chair Mario Draghi seemed to lack concrete action after he claimed the Euro will be supported at all costs, Spanish and Italian bond yields dropped and the Euro strengthened. Big money flows also show that long bonds are being bought by institutional funds despite the temporary setback in bond prices, and gold has issued a simple technical buy signal by virtue of the 20-day exponential moving average (ema) crossing over the 50-day ema on the upside. Perhaps markets are beginning to show signs that they expect quantitative easing to increase sooner than later.

But while markets may be anticipating an acceleration in quantitative easing (QE), QE has had minimal effect on the economy but has had a bullish effect on stocks. So should the pace of QE accelerate, it may have an indirect effect of eventually stimulating the economy by helping to regenerate wealth via a rising stock market.

Still, we would like to see further evidence in terms of leadership and general market action before the all clear can be sounded as the market has been rangebound and whipsaw. The S&P 500 is close to resistance as it approaches its April 2012 highs and former leaders have disappointed investors with weak earnings and/or sales projections, often a manifestation of slowing global demand, after all, the UK and much of Europe are in recession. Looking ahead, there is growing expectation that the Federal Reserve will provide some transparency regarding QE3 at the annual summit in Jackson Hole, Wyoming, August 30 - September 1. As further evidence of growing optimism, European markets and commodities markets which had been downtrending for months have reversed higher over the past few weeks.

Stocks

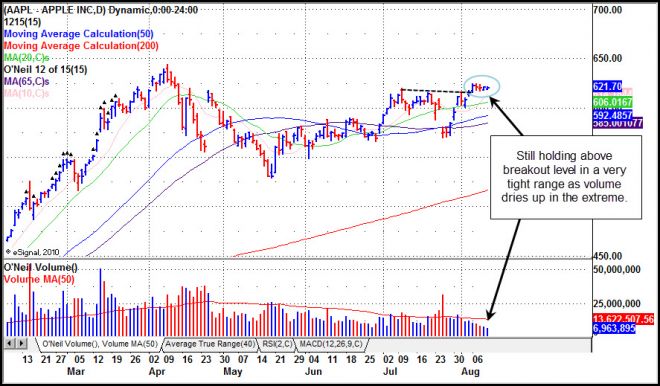

Apple (AAPL) remains in a very tight range, almost excruciatingly so, over the past five days, and while little buying interest was evident in the stock on its recent breakout through the 619.87 level the stock would not surprise us by moving higher from here. Meanwhile, leadership remains somewhat narrow and uneven, but we would look for this situation to improve if the market is indeed able to move higher from current levels.