Gold and silver are gapping up. The general market and non-precious metal commodities are gapping down. The fear factor is alive and well. And it should be, given the current fundamental backdrop.

However, the Federal Reserve meets on Tuesday. The U.S. debt downgrade that occurred over the weekend may press the Fed's hand to make an announcement regarding the start of quantitative easing (QE3). Today's gap down may thus be the market panic bottom. But picking a bottom is like trying to catch the proverbial falling knife. So while the market sorts itself out, one can either stay safely on the sidelines in cash, or continue to use our pyramiding directive with precious metals. If one sold their precious metals holdings last week on the short term reversals seen in gold and silver, one could buy back part or all of their position in either SLV (1-times silver ETF) or AGQ (2-times silver ETF) at around where they were sold on Thursday's reversal, given where silver is looking to gap up at today's open.

On the other hand, if the market continues lower over the short term, in a partially-equivalent manner to what it did in late 2008, the market may take precious metals lower as margin calls are met, much as the market did in late 2008, where nothing was profitable except the short side (or in inverse ETFs).

Another precious metals buying strategy is to use today's high in silver (SLV) and gold (GLD) as your buy or pyramid point. In other words, buy/pyramid SLV and GLD only after today, but only after they move above the intraday highs they each set in today's trading. If this is an additional buy, your average cost should be a fair degree lower than where either gold or silver are trading. If this is your first buy, position size appropriately so if you are forced out, you lose little. Then as silver and gold continue higher, add to your position as each precious metal proves itself on a price basis.

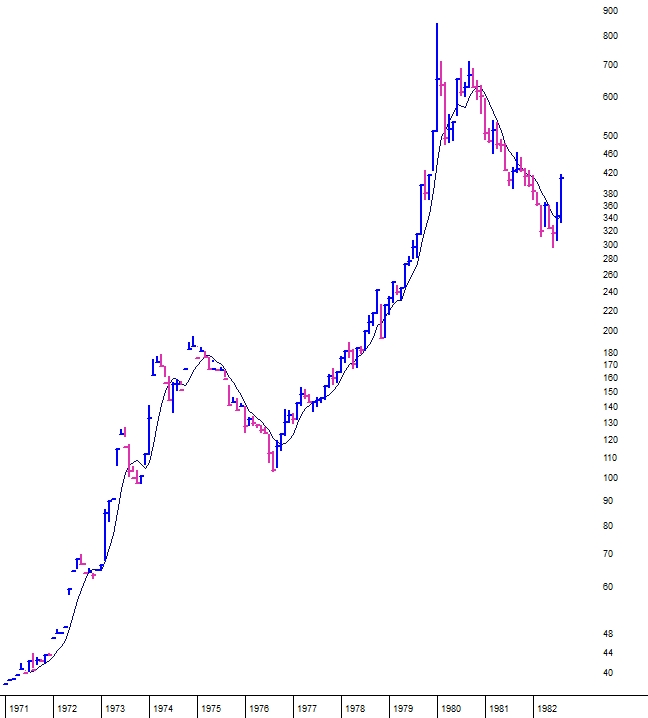

Here is an interesting historical sidebar on the price behavior of precious metals in the 1970s. Inflation increased through the end of 1974, correlating with a huge rise in gold from around $50/oz to $195/oz by the end of 1974. Inflation then fell and gold corrected for a year and a half. Inflation started up again in 1977 as measured by the CPI. Gold found its low in mid-1976, then staged a fierce uptrend all the way through Jan 1980. Non-precious metal commodities also correlated with the move in precious metals.

Figure 1 = Price of gold 1971-1982:

Hard assets including precious metals and other commodities were the leaders in the 1970s. Even collectible hard assets such as philatelic stamps did well. Stocks, on the other hand, languished due to severe stagflation and the fact that quantitative easing was not on the agenda to the degree it is in today's market environment.

Thus, in the intermediate to longer term, both stocks and commodities should move higher given the amount of quantitative easing that is to come in both the U.S. and in Europe. But at this juncture, stocks are more vulnerable, so our money remains on precious metals which have many tailwinds at their backs:

=Fiat currency printing (quantitative easing) in the U.S. and in Europe. The PIIGS are bankrupt so expect more money printing out of the ECB (European Central Bank).

=Limited spending cuts and limited tax increases via the eventual agreement to hike the debt ceiling.

=A safe haven when investors get scared the debt ceiling will not get raised.

=Demand on gold from fast growing countries such as China.

=Stagflation in the U.S. is in the offing (high inflation, low growth). As discussed above, precious metals did exceptionally well in the 1970s. Gold is not just a safe haven but also is a hedge against inflation. As more money gets printed, the further gold (and silver which correlates a good degree to the price of gold) will rise.