Market Lab Report

by Dr. Chris Kacher

The Web3 Evolution Will Not Be Centralized™

Trump and inflation

It has been argued that Trump is favorable for cryptocurrencies not because he has said so, but because it makes it easier to operate a crypto business because of the inevitably required changes at the SEC. Furthermore, under Trump, lower tax rates and tariffs are often inflationary which is good for bitcoin.

While I generally agree with this view, even without Trump, stealth QE is endless due to debt interest, unfunded liabilities, the Fed preventing Japanese banks from selling USTs, supporting the war efforts, and uneconomic climate change policies. With Trump, we may get even more inflation, but this may then prevent the Fed from lowering rates even in the face of a contracting economy. The question will be how fast the economy contracts. AI/blockchain may create so much utility it offsets any steep contraction which will give the Fed breathing room. If the utility created is insufficient, the Fed may create a reason for new QE (unlike the stealth kind) to buoy the economy. When Trump was President, he was aggressive with the Fed to lower rates. He will act in similar fashion should he be re-elected. While the Fed claims they are not a political body, they can always "invent" reasons to justify QE.

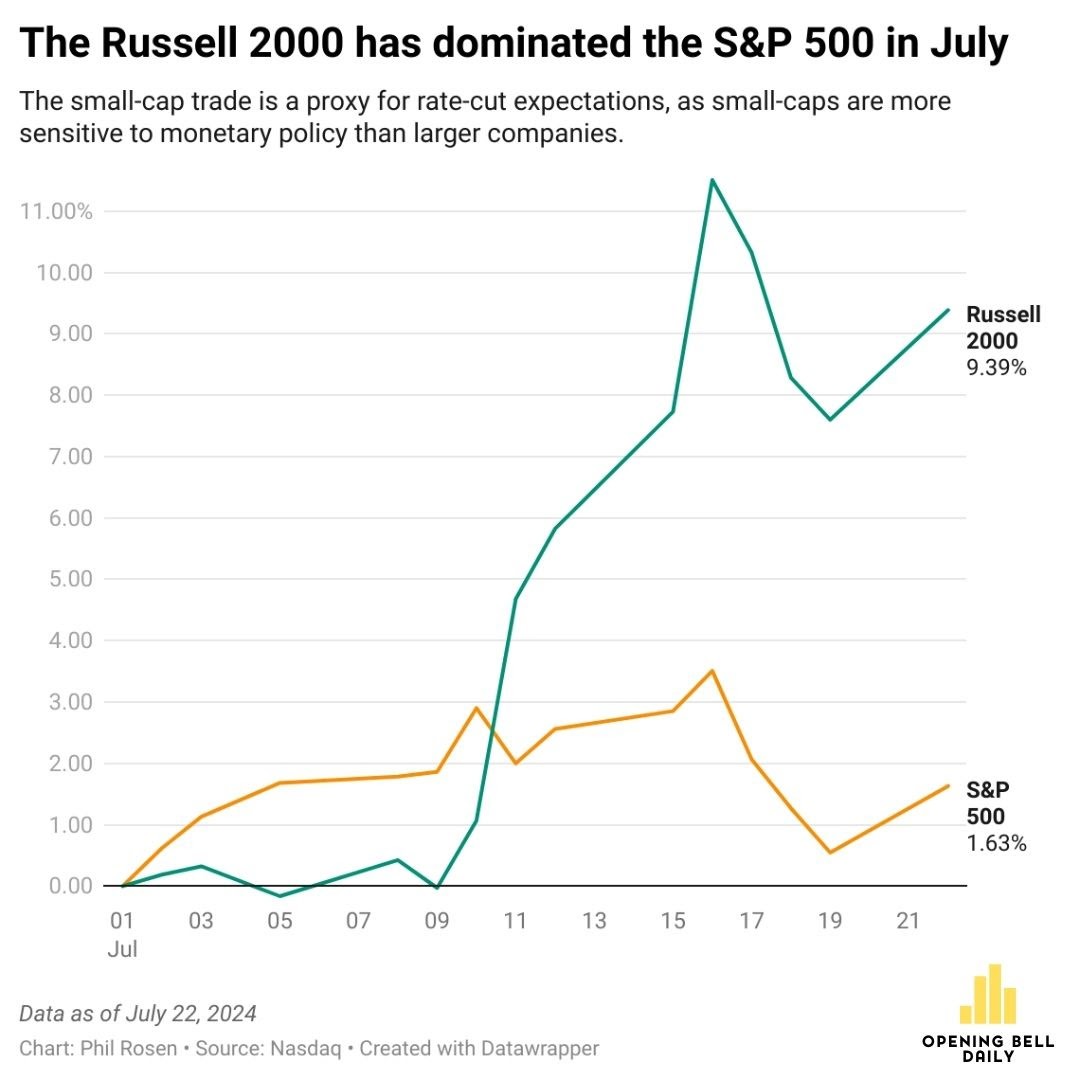

Biggest performance difference ever

The tech-heavy NASDAQ Composite and the small cap Russell 2000 had the biggest performance gap on record going back three decades. Trump winning the election favors small businesses with lower taxes. Odds are also tilting in favor for a Republican sweep across the House and Senate.

Big Tech names had huge earnings beats in the prior quarters. JPMorgan’s strategy team told clients they expect “another monster quarter.” Estimates put the S&P 500’s earnings growth at 9.7% for the second quarter, which would mark the highest annualized figure for the index since the end of 2021. Russell 2000 companies, by comparison, have seen weak earnings for the last five quarters thus its demonstrable lag. While estimates see small caps reporting improved profits in the latest cycle, it’s unlikely to be enough to maintain the recent stock rally in small caps. But with more liquidity on the way and strong earnings for large cap tech stocks, markets could continue to trend higher after the brief pause we have witnessed as the NASDAQ Composite and S&P 500 are well overweighted with big techs. Of course, this Friday's PCE and next week's jobs report and Fed testimony will be closely watched as key measures of inflation, economic health, and guidance.

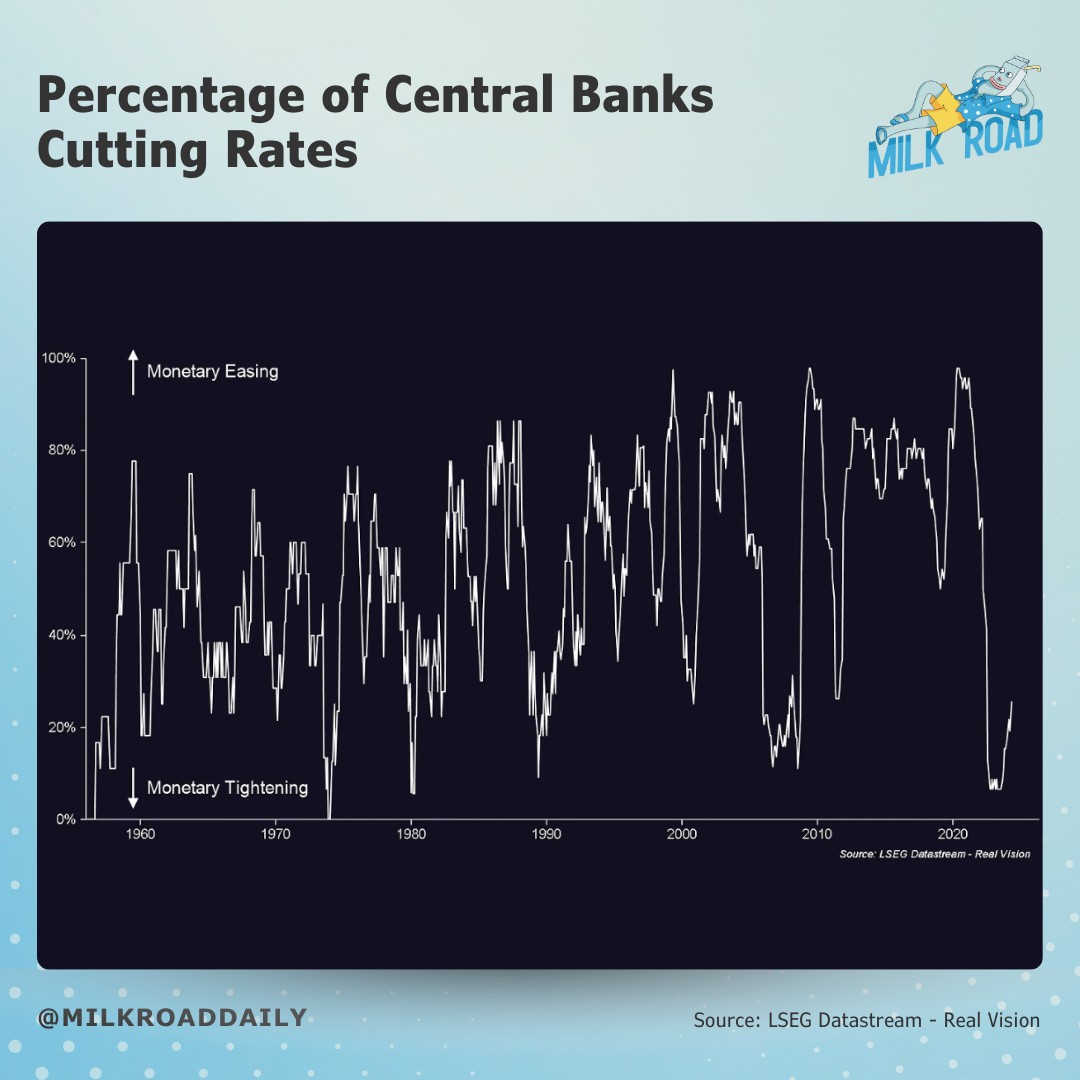

Rate cuts on the way

25% of central banks have started cutting rates meaning more liquidity. The People's Bank of China cut its one-year loan prime rate by 10 basis points to 3.35% and reduced its five-year loan prime rate by 10bp to 3.85%. This was the first rate cut in a year after repeatedly refusing to add stimulus to the economy to boost growth. The Chinese government has no choice but to support its economy in this manner.

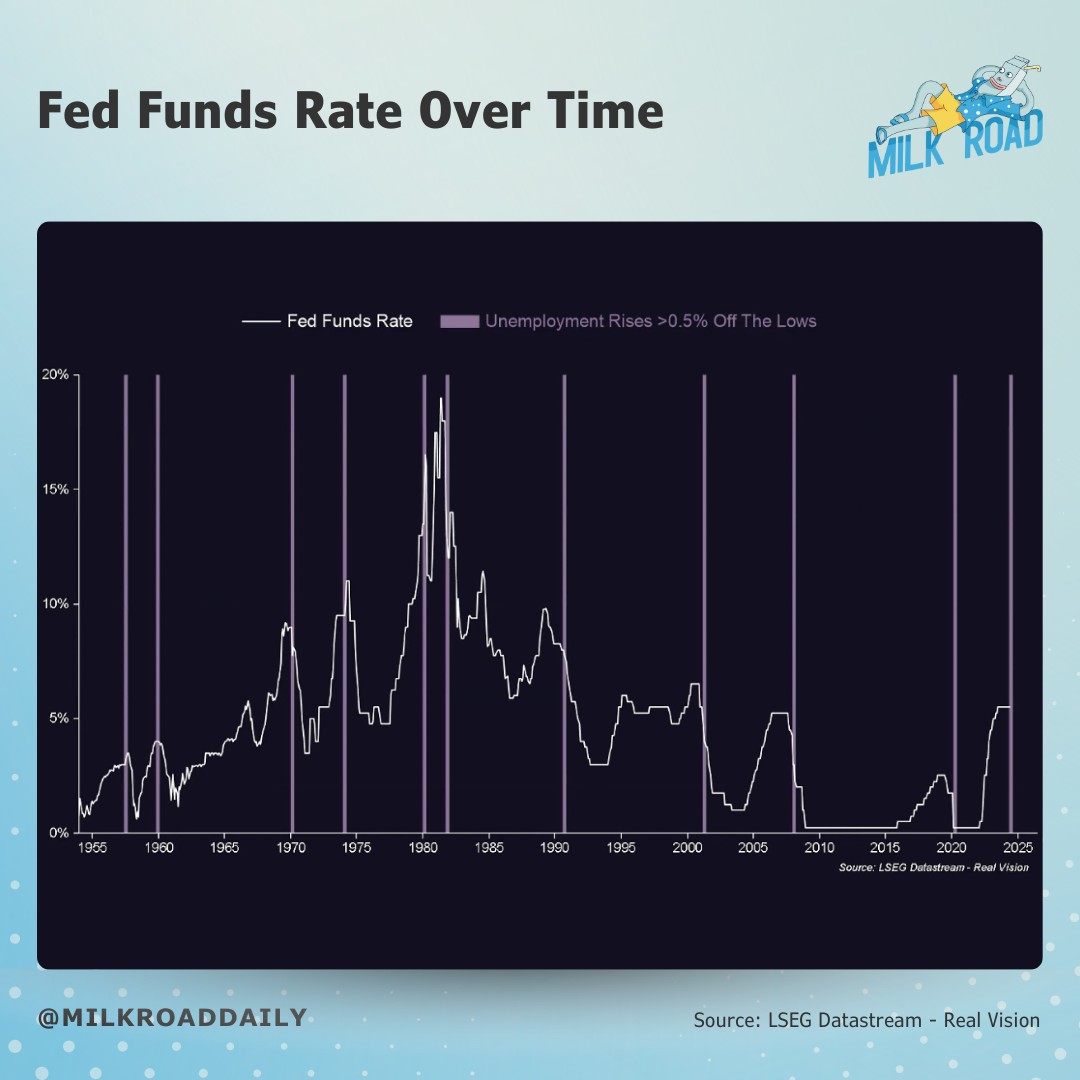

One big caveat is how bear markets began shortly after rates were cut such as in 1990, 2001, 2008, and 2020. 2008 and 2020 were cut short by QE. The Fed may not be shy about unleashing QE again should the economy start to falter. The economy did not falter sufficiently in 2022 but markets tanked because rates were hiked faster from near 0% than ever in history. This put a stranglehold on liquidity.

It is also evident that when unemployment rises by more than 0.5% off its lows which it currently has, the Fed tends to act by lowering rates. The last two times this happened was in 2008 and 2020. Both times, the Fed used QE to cut short recession. If we examine the two times before this, in 1990 and 2001, the Fed did not have QE at its disposal so both recessions were of typical length where stock markets lost a substantial amount.

The Fed has said it is still concerned about cutting too soon but has indicated that rates have come off enough that a rate cut sooner than later is warranted.

Market direction

Major averages overweighted in tech stocks were overbought so the sharp selloff due in part to a rotation into small caps is not entirely surprising. The attempted assassination was the start of the shift into small caps because the odds of a Republican Congress and President soared which favor smaller companies who normally have been the lifeblood of an economy. We still have lower rates on the way which should help liquidity which had been mostly in a downtrend this year though in the last couple of weeks has been trending higher. QE in all its forms continues the inflation megatrend. We also have massive utility from AI and an election year where a Republican Congress and President seem highly likely.

In parallel to today, late 2018 saw diminished levels of QE and slowing economies so in consequence, major averages were sloppy and trading in wide bands. For the first half of 2018, they would selloff hard then grind back up to new highs. Thus the Market Direction Model since then opted to capture wider bands as the market tended to trend higher but in a sloppy manner given the tug-o-war between QE vs. slowing economies. During these times, the model took fewer signals to capture major trends which helped minimize whipsaws. This meant being able to ride major trends longer. This is a different style to those who wish to trade the markets on a shorter term basis. Of course, one can place their own sell stop in alignment with their risk tolerance. We advise members to risk significantly less capital than normal should volatility levels become elevated. During such periods, the Market Direction Model will take greater risk by allowing larger losses during such periods to avoid getting whipsawed.

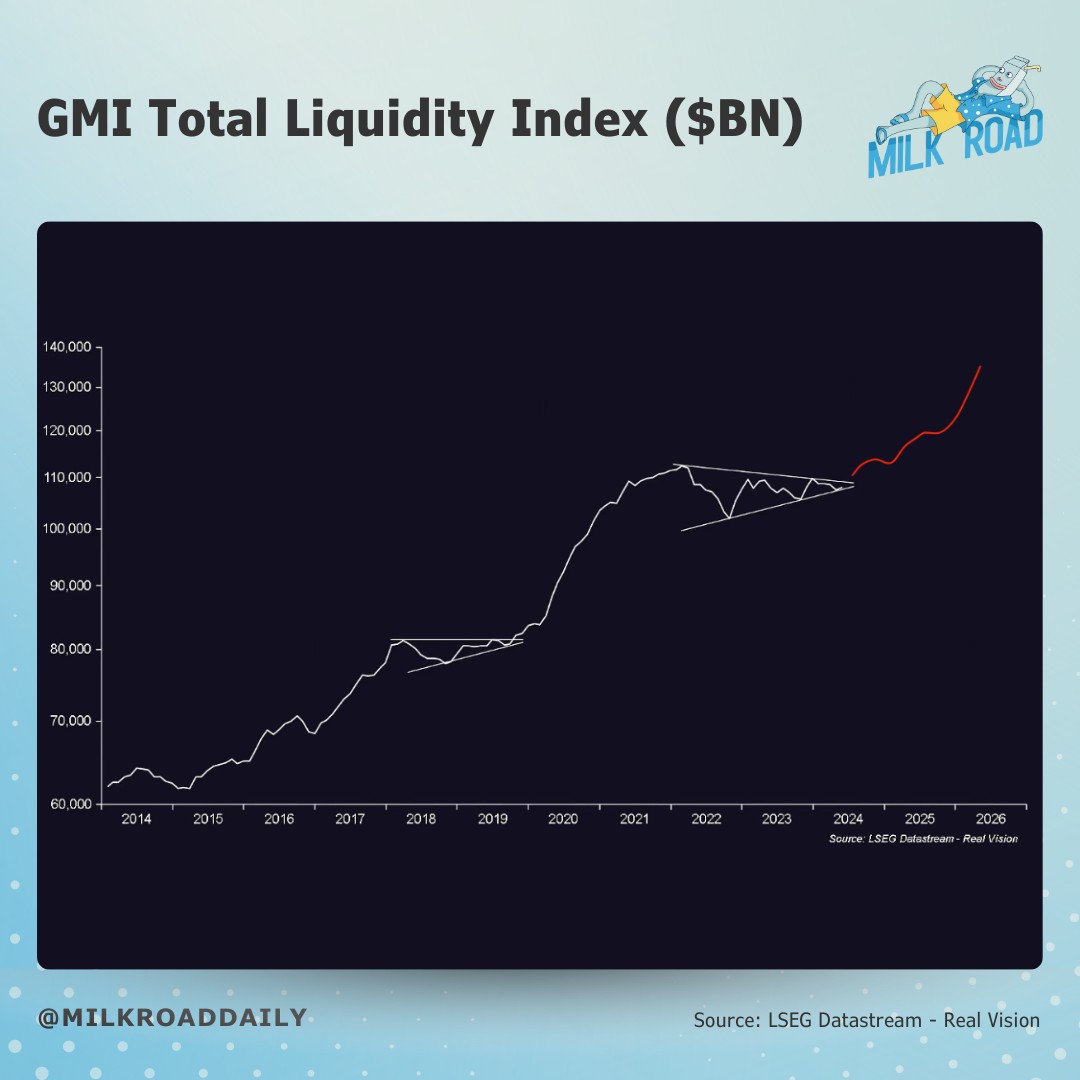

Meanwhile, lower inflation and rising unemployment forces the Fed to cut rates. CME FedWatch is pricing in three rate cuts by the end of this year. In consequence, a very telling chart of global liquidity suggests it will inevitably rise. So while the amount of global liquidity has slowed in 2024, it is likely to start trending higher later this year given the countless reasons central banks will need to print more fiat. We will keep a close eye on this metric and advise accordingly.

ETHE spot ETFs

On the day the bitcoin spot ETFs were launched in January, BTC sold off. This persisted for a couple of weeks before bitcoin found its floor. This selling was due to holders of GBTC who could finally sell once the spot ETFs were launched. The same thing seems to be happening with the ethereum spot ETFs. You can track inflows into the new spot ETFs and outflows out of the Grayscale ETHE vehicle HERE.