Market Lab Report

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

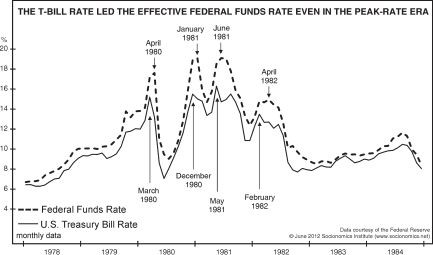

Stock market leads 3-mo Treasurys leads Fed Funds Rate

I showed a chart in a prior report where the Fed Funds Rate typically follows stock market direction, and also equates well with the rough principle of "Three steps and a stumble" where the Fed hikes a few times, which then ends the bull market, forcing the Fed to then lower rates. The US 3-month Treasury is also a solid predictor of the direction of interest rates. While the stock market leads the FFR, 3-mo Treasurys lead the FFR. For example, T-bill rates peaked four times in 1980-1982. Each of those peaks occurred a month or more before subsequent and reactive peaks in the federal funds rate. The Fed's rate also lags at bottoms, as depicted on the chart at the lows of 1980, 1981 and 1982-3.

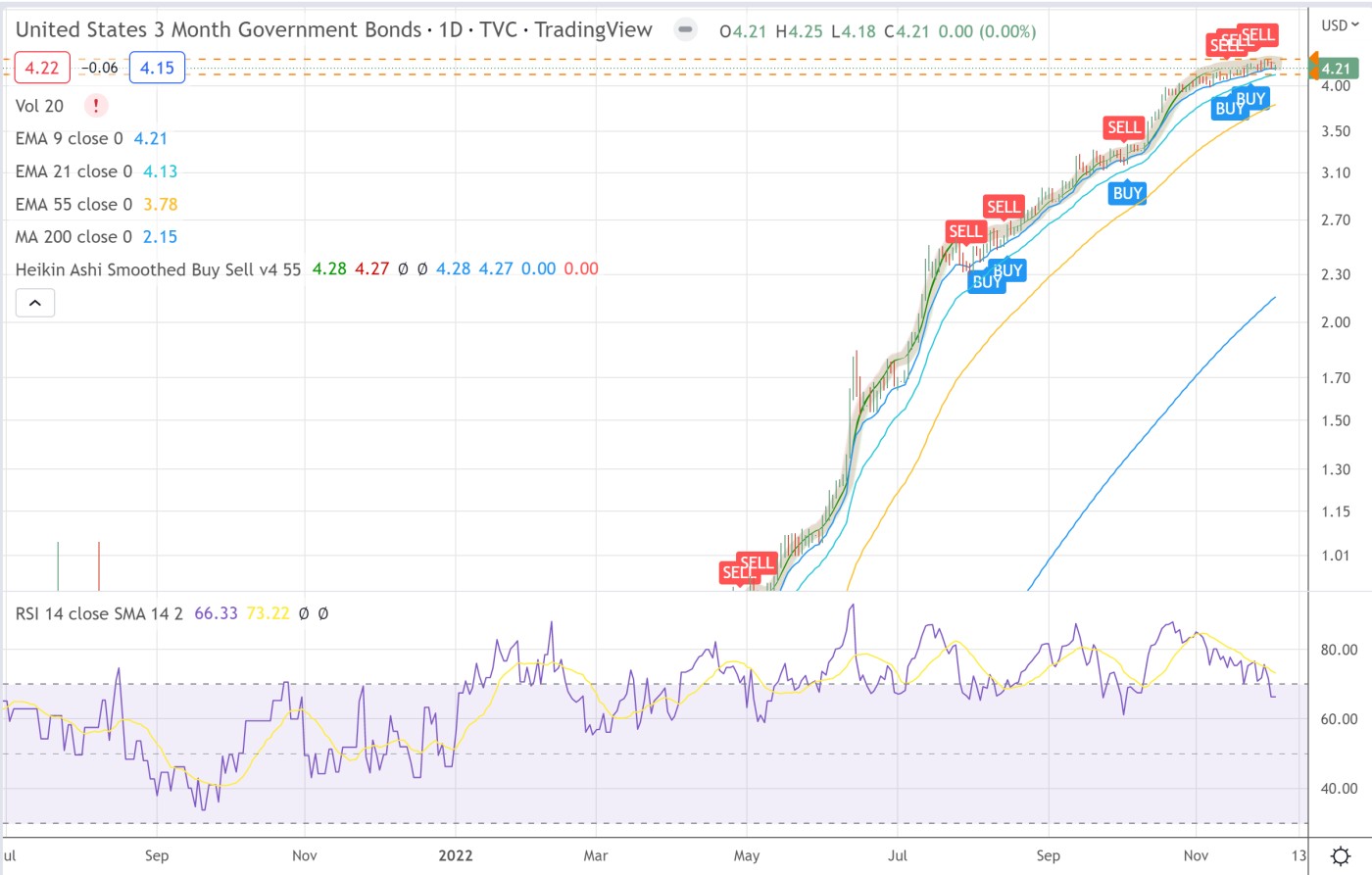

According to various including Goldman Sachs, inflation is likely to stay stubbornly high, well above the Fed's 2% target, so rates are also likely to stay elevated. The CME Fed Funds futures predicts the FFR will remain at 475-500 bps until late 2023. While inflation may soften to around 4-5% over the next couple of quarters, it gets much harder to reduce inflation below this point due to supply side limitations. As we have written, the Fed does not have the tools to fight supply side inflation. They can just hope demand sufficiently cools so that the demand side of inflation drops.

Meanwhile, Powell's dovish words last week has given the recent dead bat bounce more upside momentum. But the Fed has already made it clear they must reduce inflation down to their 2% mandate so they must continue to hike rates. This will induce a severe recession (unless we get a black swan, see below) since they cant have it both ways, ie, they cant have a soft landing by pivoting AND at the same time, reduce inflation down towards their 2% mandate. But then, the Fed has made such misstatements numerous times in the past. Remember when Powell said inflation is transitory back in late 2021? Then remember when the Fed said we are not in recession after two quarters of negative GDP growth on the basis that the jobs market is still strong?

Powell is not stupid so he's instead become a mouthpiece for market manipulation. He must know that unemployment is always at its lowest before it soars and recession begins. I published results showing exactly this behavior in what became an infamous study in the year 2000 where I called for recession in 2001. The study was denounced by Wall Street because I was the first to use the 'R' word while Wall Street is all about bull markets which keep customer interest and sales strong. What I showed then still is true to this day.

So expect soaring unemployment, a deep recession, and both stock and crypto markets retesting and plumbing new lows in the months ahead unless we get another major black swan. We had the first x-mas crash on record on Dec 24, 2018 which forced the Fed to stop tightening their balance sheet. Not coincidentally, that was the major market low.

Because of the interconnectedness of major financial elements, the odds of a black swan that forces the Fed to print trillions once again are greater now than ever, though there are no guarantees, and the odds are still small, though not minuscule. Black swans are supposed to be very rare events, but we had one in 2000 with the bursting of the dot-com bubble, then in 2008 then again in 2020. Perhaps in today's world, black swans are only just "unusual".

If we dont get a black swan, the S&P 500 has never bottomed before a recession since WW II, so expect the recession to be materially worse than a typical recession because we are in one of the worst macro environments on record due to record levels of debt, persistently high inflation due to supply side issues born from COVID and political unrest, and historically low interest rates which have forced the Fed to hike rates despite downtrending markets. As I illustrated earlier, this is a first for the Fed as they normally follow the stock market with their interest rate decisions. This time is indeed different.