by Dr. Chris Kacher

QEndless

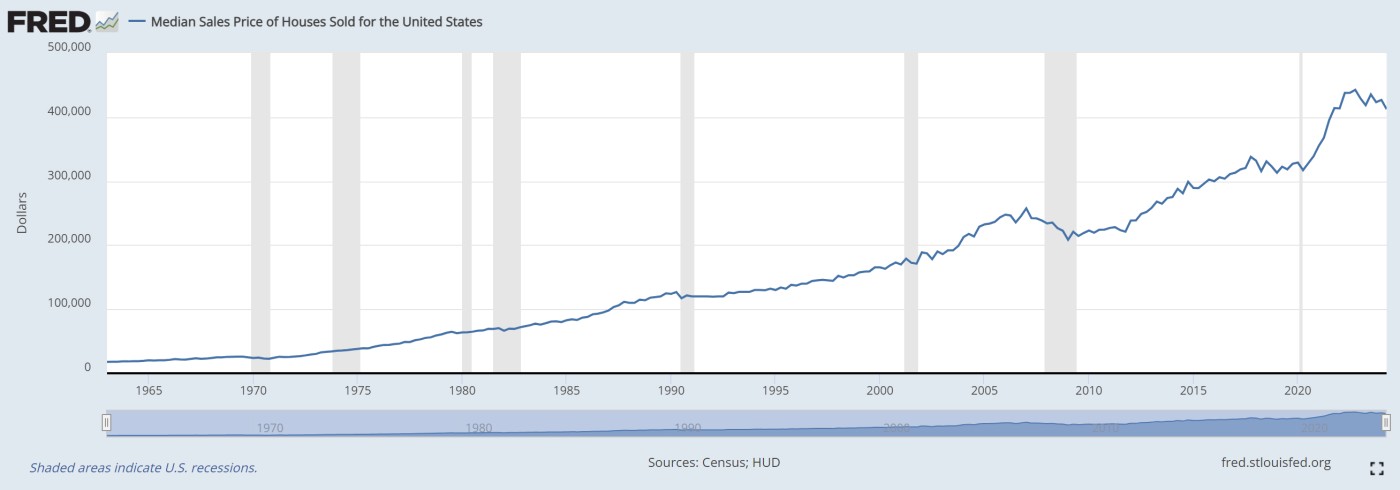

QE in all its forms is driving the inflation megatrend. This is why stocks and real estate tend to trend at a faster rate since 2008 when QE was first launched. Meanwhile, real estate housing prices in the US have jumped 25-fold in the last 60 years, and up as much as 40% since 2020. This implies the dollar's value has fallen 96% in 60 years based on this metric. A dollar buys you 4% of the median house it used to. This has contributed to the statistic that one in eight families in the US are millionaires. The top 12.5% of homeowners are sitting on homes now worth over $1 million.

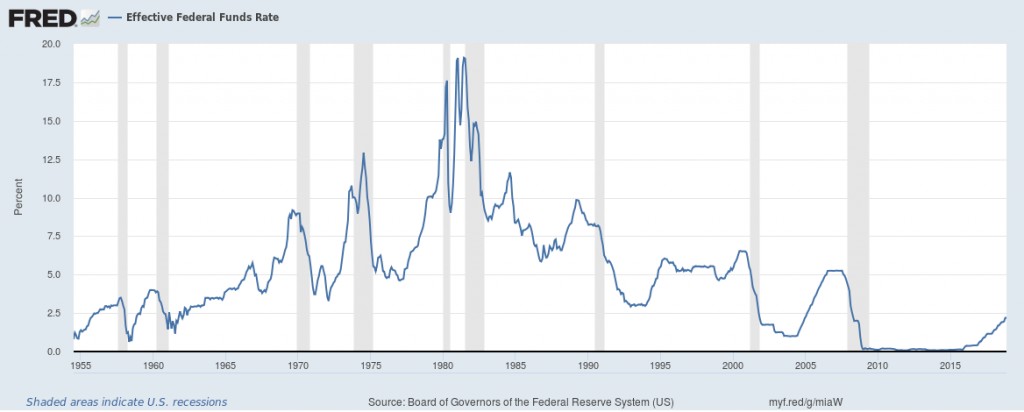

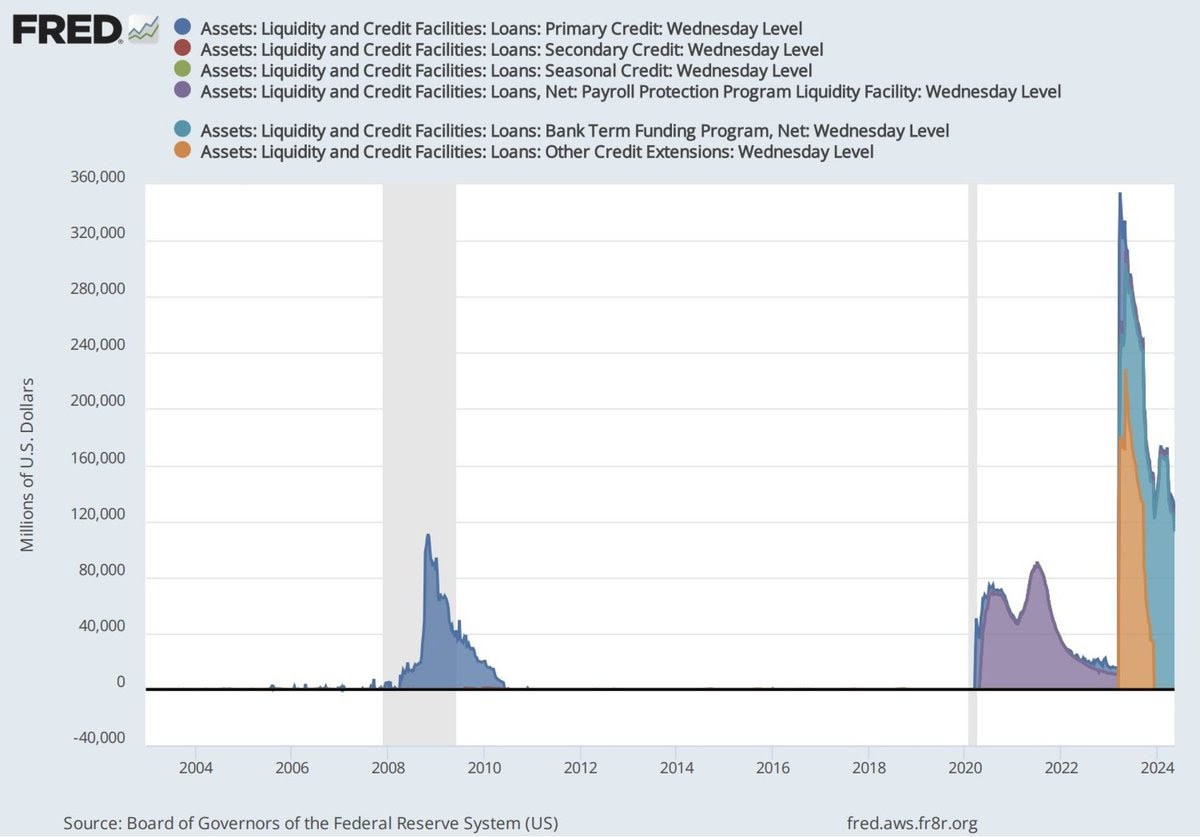

The QE money train will not stop. The Fed made more emergency loans in 2023 than during the financial crisis of 2008 and during COVID of 2020. We had one of the largest banking crises in 2023 because the US government first sold billions in bonds to financial institutions then devalued them by hiking rates at the fastest pace in history from near zero levels.

The blue bump below on the left is the lending from the global financial crisis of 2008, the purple bump is COVID, and the orange/aquamarine monster on the right is the 2023 banking crisis.

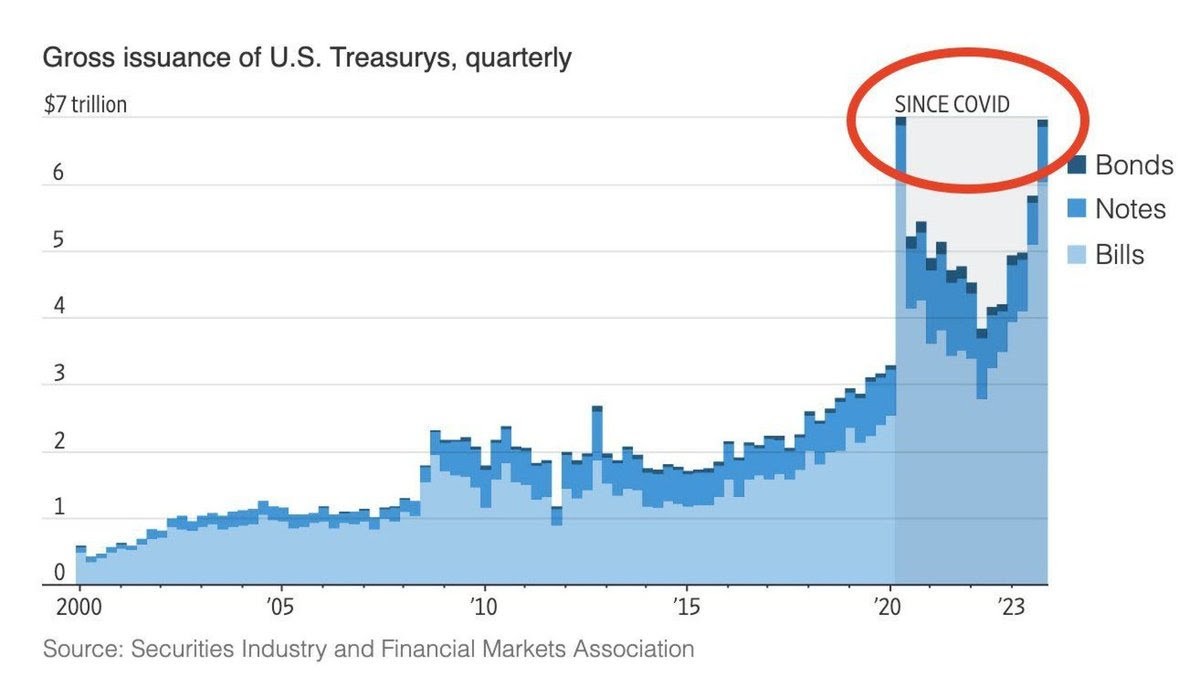

The US government also borrowed more under the "Biden boom" than it did during COVID. COVID borrowing was at ~0% rates but today's borrowing of historical sums of money is at 5%.

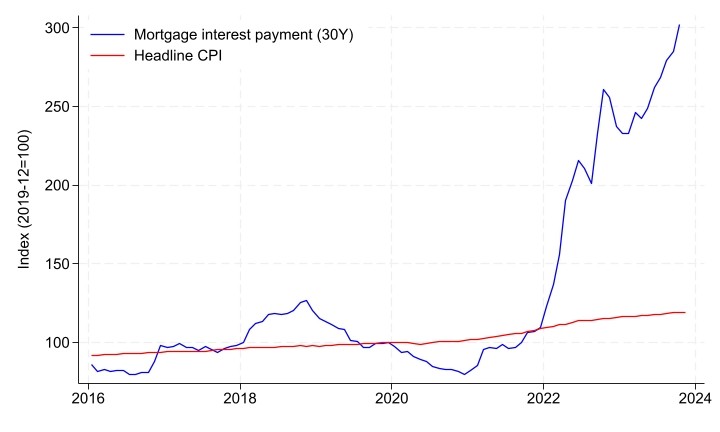

Pre-1983, mortgage costs were included in the CPI as were car payments pre-1998. Today, the CPI does not include borrowing costs. So when interest rates jumped starting in 2022, official inflation figures did not fully capture the effects it would have on consumer well-being.

In consequence, the dollar has lost at least 25% of its value in just four years. Larry Summers estimates that purchasing power has been eroded even more radically than this, with annual numbers hitting 18% if you include the enormous spike in loan payments due to rate hikes. Compounded over four years, that would be easily more than 25% of the dollar's value. Thus stocks, real estate, bitcoin, and certain hard assets have all benefited greatly.

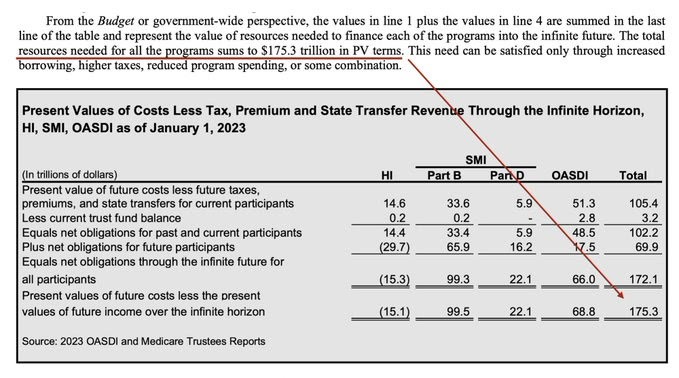

The true debt of the US is $175.3 trillion when you take pensions, medicare, and social security into account. This number is itself rapidly increasing. US national debt just topped $35 trillion, and the US Treasury boosted liquidity buyback to $30B from $15B. Stealth QE, also known as "Not QE 2.0" is growing.

That $175.3T lines up with the ~$200T number that Stanley Druckenmiller has been using for the all-in liabilities of the US government when you take everything into account. The dollar continues to sink, only $2 trillion was collected last year by the federal government, that number is artificially boosted by deficit spending, and if there is an accelerating loss of confidence in the dollar, this $175.3T in asset value will drop if liquidated.

In short, the US government doesn't have nearly enough to pay for what it owes. It would have to grow its way out of this massive debt as it did post World War 2. Only the enormous utility created by cutting edge technologies such as AI can save the day. But the odds of this happening are becoming questionable at best. While generative AI is growing at breakneck speeds, it still takes time for its effects to sweep through companies in a way that is fully transformative. If a debt crisis occurred, this would force the Fed to fully relaunch QE in all its infamy. But should that occur, the amount of money created would make prior crises seem small which would in turn accelerate the devaluation of the dollar.

The recent shift in market sentiment from large to small caps is due to the high likelihood of a republican congress and presidency where smaller companies benefit thus the exodus out of well overbought big techs and into small caps. We are seeing a slowing economy as we did in 2018 which saw market whipsaw pullbacks in the first half of the year only to bounce back to new highs. But back then, the Fed was tightening whereas today, loosening of monetary policy is at hand. We also have a substantial amount of stealth QE due to interest payments on record levels of debt among many other matters.

Meanwhile, AI stock AMD gapped higher due to a strong earnings report and NVDA gapped higher at the open due to MSFT saying they would accelerate AI-infrastructure spending which will boost Azure's ROI. In consequence, NVDA investors are "counting on Microsoft to be [the company's] biggest customer this year" for graphics processing units. Other major tech juggernauts such as AMZN and AAPL may also indicate a boost in their AI-infrastructure spending when they report earnings much as META indicated after Wednesday's close.