Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

Global liquidity

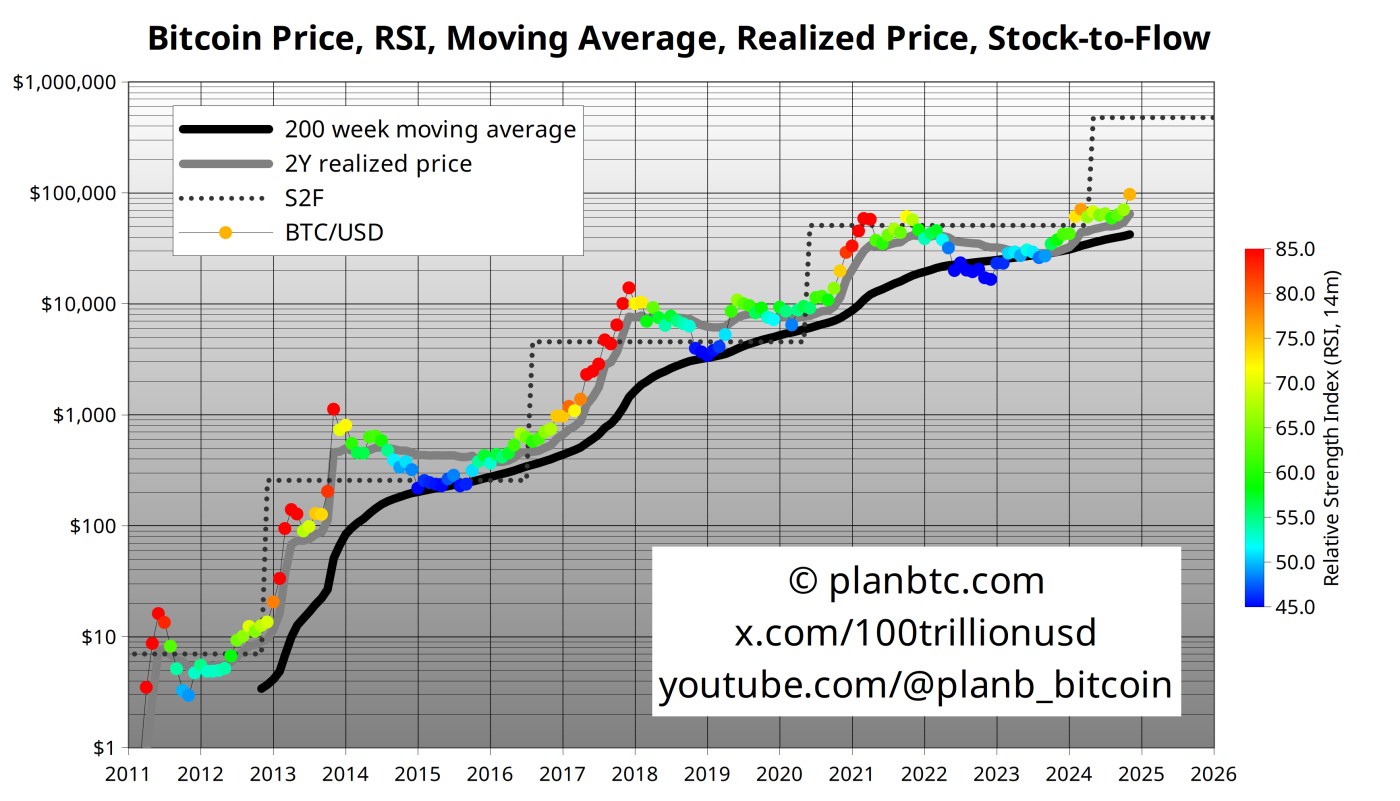

See those red dots which signify when RSI>80? In the past, when bitcoin goes red:

2017: bitcoin pumps 10x from 1k to 10k

2021: bitcoin pumps 3x from 20k to 60k

2025: ?

Helping Bitcoin move from yellow to red is global liquidity. Some are concerned that the US market is currently selling for 28.4 times trailing earnings, but that is still a long way from Japan’s extremes at their mega top in 1990. Similar fingerprints of abundant liquidity are evident, and indeed, it is true that Powell and Yellen have been engaged in stealth QE, probably in the failed hope of helping Biden’s re-election bid, but it's the flood of foreign capital that makes the largest difference. So expect markets to continue to enjoy the wave of liquidity as fiat debases and BTC eventually reaches well into 6-figure sums as long as the current environment holds up, ie, global nuclear war is averted and inflation does not soar forcing central banks to reverse their rate cuts.

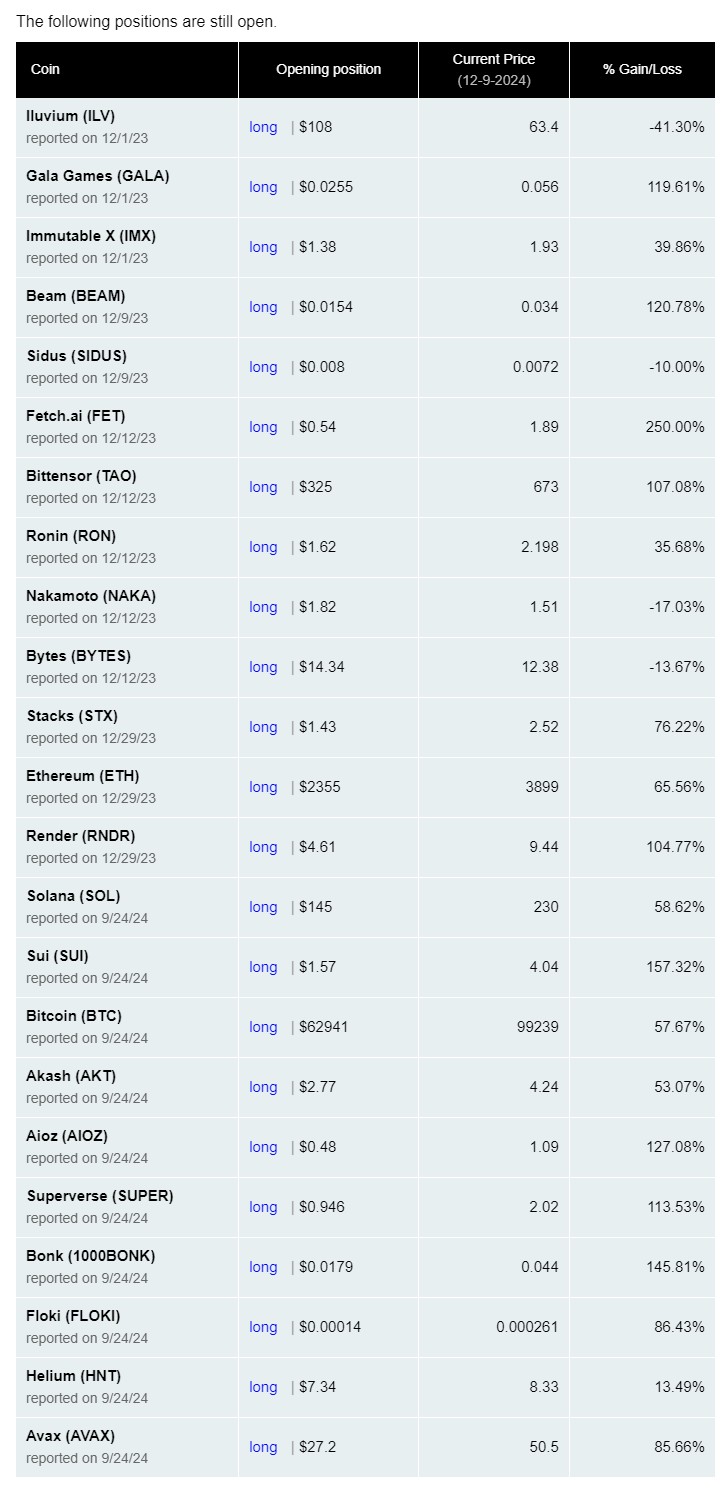

Meanwhile, altcoins are just getting started.

My altcoin picks have done well as an aggregate but keep in mind that position sizing is key as strength begets strength so the ones that lag should be halved or sold where the capital is placed into the performance leaders, thus % gain/loss has little meaning compared to how one positions their portfolio. I have always at least halved positions multiple times or sold them outright if a stock or cryptocurrency lagged the rest of the portfolio.

Inflation vs economic strength

The US added 227,000 jobs in November, higher than the forecast for 214,000, but the Labor Department also reported unemployment ticked up to 4.2%. So there's more softness in the job market which argues for more rate cuts but wage growth is running faster than in the pre-pandemic period that could pressure inflation higher which argues for a slower pace of rate cuts. So the economy shows resilience but the labor market is weakening. While inflation is moderating based on the distorted data pushing central banks including the Fed to lower rates, QE will eventually send inflation higher. It is only a matter of when, not if.

While the CPI is ticking higher once again, the Fed will likely cut rates not because of the economic data that shows a strong labor market and rising MoM and YoY inflation but because they don’t want to surprise markets. This flies in the face of history prior to QE when the Fed would raise rates to curb excessive price growth. The new target of 3% inflation has arrived.

Overvalued markets/current investor sentiment

Overvalued markets and current investor sentiment are at multi-year highs. Individual investors are showing unprecedented confidence in the stock market, with 46% of U.S. investors believing there's less than a 10% chance of a market crash in the next six months, marking the highest confidence level since June 2006. This optimism has doubled over the last two years, according to a survey by the Yale School of Management. Concurrently, the S&P 500 has rallied by about 50% since its low in October 2022. However, this optimism is juxtaposed with the belief that the market is the most overvalued since the Dot-Com Bubble in April 2000, suggesting a euphoric market sentiment.

But QE has changed the situation. The focus on price inflation due to QE missed the significant asset inflation that followed. There's a debate on whether asset bubbles will burst or if central banks can keep inflating them indefinitely through monetary policies like QE. The Fed's use of QE has fundamentally altered market dynamics. The Fed can quickly cut rates and print money, leading to a scenario where asset prices might never experience prolonged downturns, as exemplified by the rapid recovery post-2020 market crash and the Silicon Valley Bank collapse in Mar-2023. The Fed now acts in response to market expectations rather than leading market behavior. This was evident when Ben Bernanke's Fed had to adjust QE to meet market expectations to avoid asset price drops.

Investors face a choice between continuously fearing an upcoming bear market as has been the case for a number of years or acknowledging the new financial regime where the Fed consistently supports asset prices. Investors should consider the long-term effects of central bank interventions, especially QE in all its forms, which have arguably made the market less about timing and more about staying invested over time. The choice for investors is to either be skeptical of this "new normal" or adapt to it, viewing market dips as opportunities for buying due to the Fed's likely response to support asset prices.

Time in the market is more important than timing the market as illustrated by the astounding performance of 3x ETFs such as TQQQ and TECL which soared 434x in 15 years. That said, I time these using a host of weighted metrics which further improves performance since one would have been in cash or short in years such as 2022 along with other bearish periods where the macro slowing of QE occurred.