Market Lab Report / Dr. K's Crypto-Corner

by Dr. Chris Kacher

The Metaversal Evolution Will Not Be Centralized™

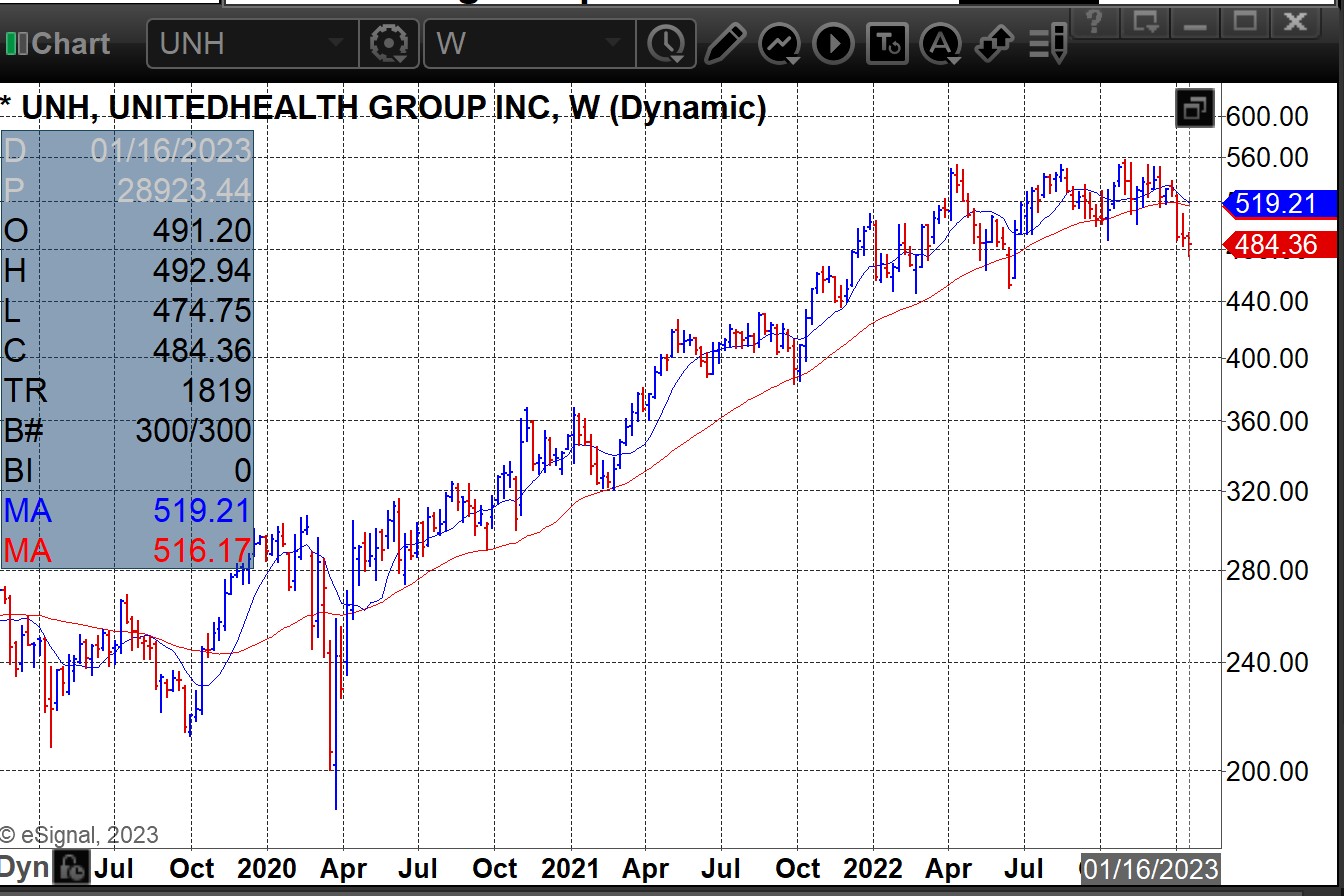

Earnings projections by companies remain bullish and unemployment remains near record lows at 3.5% while wage pressures remain low. But this is the calm before the storm. Earnings projections by companies remain bullish because this is a lagging indicator. But major names such as United Healthcare (UNH), Johnson & Johnson (JNJ), and Proctor & Gamble (PG) are starting to report disappointing earnings results. UNH is breaking down well below its 200-dma for the first time since the COVID crash in 2020. It is only a matter of time before other companies are forced to lower heir earnings projections. Layoffs from major companies such as Google and Apple continue.

Major markets remain below their 200-dmas. Lower highs and lower lows remain on course. Big tech stocks have lost 1/3 to 2/3 of their values in this bear market. Risk-on indices such as the NASDAQ remain weaker than the Dow Industrials. No new bull market is led by risk-off indices such as the DJIA.

Despite rising rates, global M2 increased in the fourth quarter of 2022 due to countries such as China who are increasing their M2's. This could create inflationary conditions in those countries which could then spill over into the rest of the world.

In addition, the Fed has ways to print money in "stealth" fashion despite the tightening environment much as the Bank of England did in late 2022, call it "QE-Lite". This suggests that despite the possibility of persistently high inflation, QE-lite can continue to service the record levels of debt. This could result in a choppy, sideways, go-nowhere market where no material trends occur in either direction.

But it is more likely that as recession takes hold, markets start into new downtrends, and the Fed is forced to pivot by halting the hikes then reducing rates. If history is any guide, markets will continue lower as rates fall. This was the case in major bear markets where bubbles had to be unwound such as during 2000-2002 and 1930-1932 among other bear markets.

The other scenario is a black swan which forces the Fed to launch QE5. This could restart the bull market depending on how much money is printed.

This dead bat bounce could continue until one of three possibilities:

a) signs of a strong economy which ups the odds for more rate hikes

b) signs of a crumbling economy create fear

c) signs of persistently stubborn inflation in the CPI, PCE, or wages

Up until now, none of the above have been sufficient to push markets lower. This suggests bad news is good news as major indices recalibrate from oversold to digest the recent positive news on inflation. But this is unlikely to last. Lingering supply chain issues and wage pressures are likely to keep inflation stubbornly well above the Fed's 2% target.