by Dr. Chris Kacher

MDM

Just a reminder that sell stops are always suggested whether it is a stock or an ETF. For the model, 6% on NASDAQ Composite and 18% on TECL had been suggested, but members often set their own stops based on their risk tolerance levels and position size accordingly whether it is a stock or an ETF. Expect high volatility so position size accordingly.

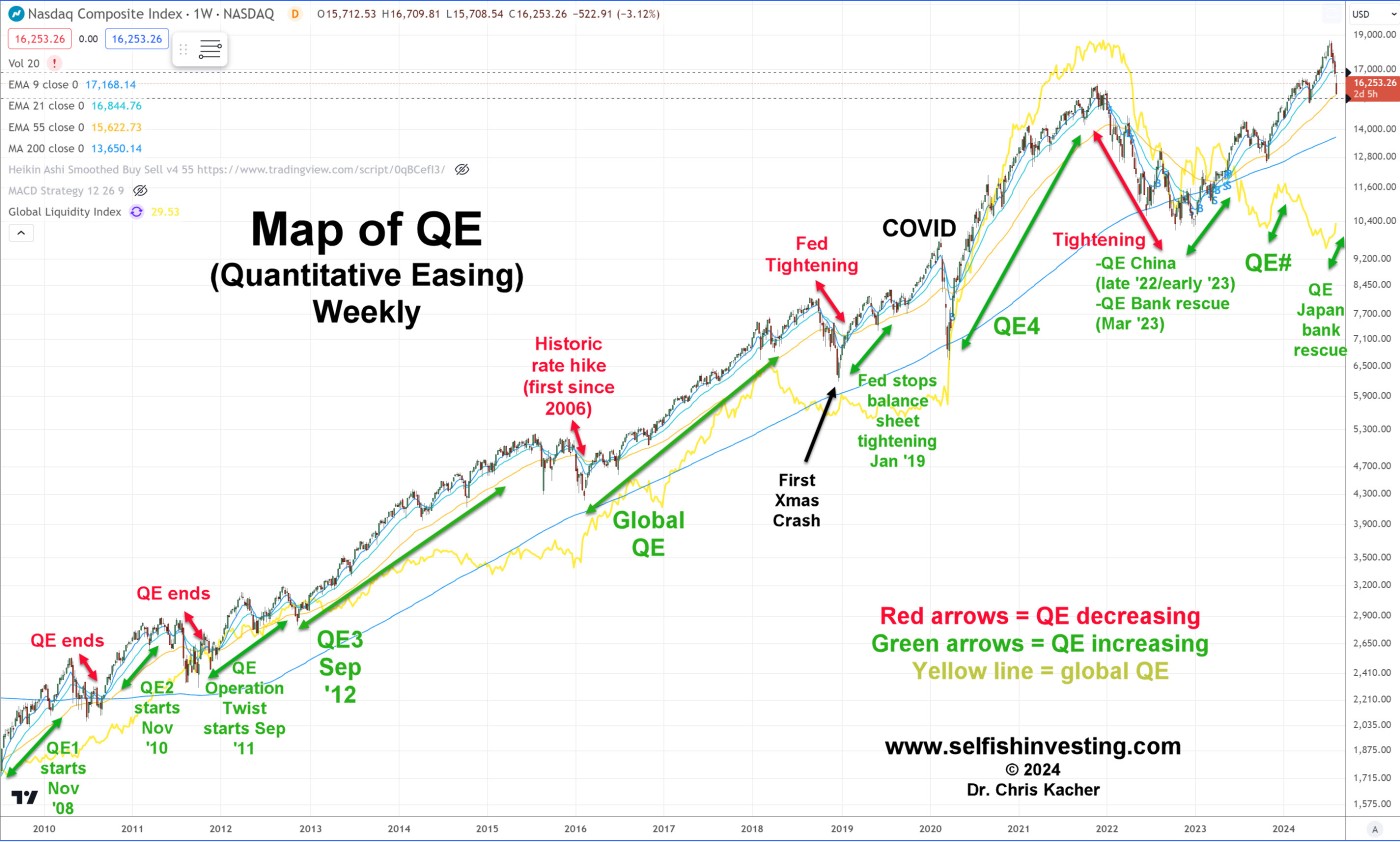

In this Era of QE, since late 2008 when QE was launched, the steeper the drop, the greater the upside since tech-driven major averages always hit new highs often within a few months of the typical 'V' bottom. To prevent whipsaws due to a slowing economy in the first half of 2018 (much as we see today), the model made a change in 2019 to sit longer on buy signals with the tiny risk of the market getting away from the model on a buy signal. It worked well until now where a cascade of negative events then the one-off in Japan created a global crash with the Japanese Nikkei having its worst two days in the entire history of its market. This pulled down global markets. Thus sell stops have always been advised.

The Map of QE shows why 'V' shaped bounces are typical though next the lows, volatility often spikes then can respike as negative news works its way through. In past VIX mega-spikes, QE was initiated. Today, the slowing economy, the Iran-Israeli situation, and any further yen carry trade unwinding will create downside volatility. It is a question of how much QE will be utilized. In past corrections, a sufficient amount was used for markets to quickly find their floors. Since 2008, only when QE slowed, ended, or tightening occurred did markets have prolonged downtrends. We are in the opposite situation today where global QE is shooting higher.

I have been doing research on the macro QE environment vs. major US averages since QE was launched in late 2008. In 2008, the NASDAQ Composite lost 51% peak-to-trough. But then it formed a "V" bottom with one retest when QE was triggered in late 2008 wherein it fiercely rallied to recover losses with the NASDAQ up 46% in 2009 and 79% trough-to-peak. Similar happened in 2018 with the first Xmas crash on record then again during COVID where new highs were made in both cases within a few months after steep corrections.

As some have been doing with success over the last decade, one can start buying the further major indices fall then, as they make new highs, one starts to slowly take profits. It's an entirely different dynamic but suits some investors' risk tolerance preferences. Some use the Market Direction Model in this manner so if its losses exceed a certain amount during a buy signal, they first sell their position then start to slowly buy if the market continues to fall even if the model goes to a cash signal. Likewise, they start to take partial profits as the market continues to make new highs on a buy signal. Since markets inevitably bounce or top, this is a way to increase profits on selloffs since during macro-favorable times, the model is far more likely to go from buy to cash back to buy as it did through most of 2020 and 2021 with virtually no sell signals.

The unravelling of Japan

The recent plunge in markets will go down in history. While Japan's stock market posted its biggest 2-day drop in its history, South Korea halted all sell orders on their stock market. Triggering the crash of world markets and spurring the recent sharp rise in global liquidity (QE/GMI) is the yen carry trade which is in the many trillions wherein an investor borrows in a currency with low interest rates, such as the yen, and reinvests the proceeds in a currency with a higher rate of return. The selloff in equities was caused primarily by a soaring yen. Borrowers then had a higher loan outstanding with a higher rate of interest. The result caused some traders to sell their assets and repurchase yen in order to pay back their loans. But that buy pressure on the yen sent it up further which forced more buying resulting in a liquidation cascade. Furthermore, marekts had priced in additional rate hikes until the Bank of Japan said they would stop hiking rates. They now know they can’t hike unless they want to cause another collapse from leveredged yen carry positions.

Since Jul 11 when the selloff began, there has been a strong correlation between major stock markets and the USD/JPY chart. USD/JPY bounced hard on the Fed's pledge to continue to make Japanese banks whole via stealth QE's FIMA repo facility since the US cannot afford the yen carry trade to unwind as it did.

The FIMA repo facility was created by the Fed in March 2020 during the COVID crash. It allows foreign central banks to temporarily raise dollars by selling US Treasuries to the Federal Reserve's System Open Market Account and agreeing to buy them back at the maturity of the repurchase agreement. It is a powerful form of stealth QE. Japan has been one of the largest buyers of US Treasury debt, or at least they were, until the yen carry trade began unwinding. To prevent Japanese banks from selling US Treasuries which would cause interest rates to rise, Japanese banks are being given capital via the FIMA repo facility. The US cannot afford further deep unwinding of the yen carry trade so will print what is required to keep Japanese banks whole. The amount could range up to or beyond $1 T between now and year end. This is in addition to the $2 trillion already pledged for this year for other expenses.

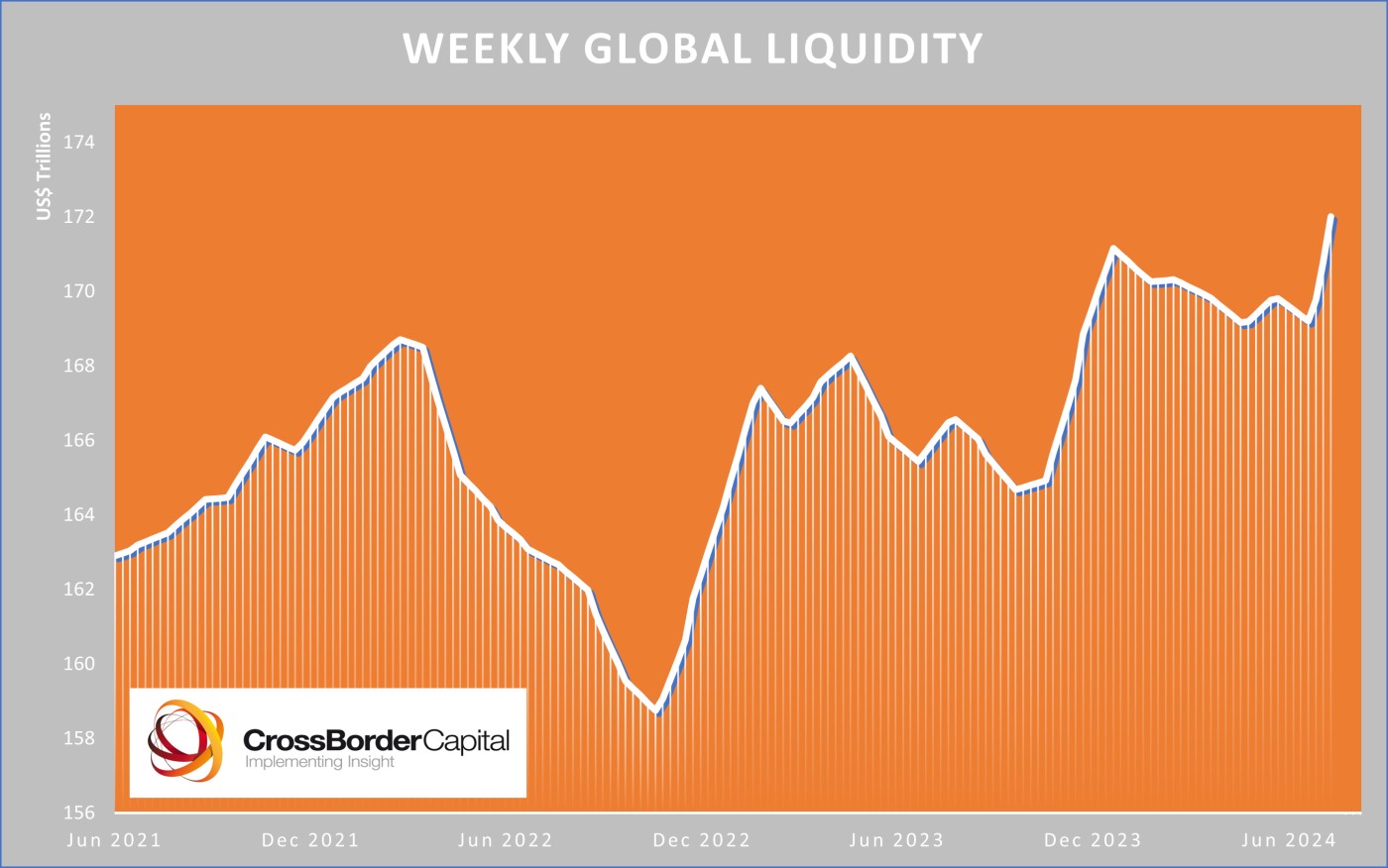

Even before the crash, renewed global liquidity was already on a sharp rise especially when accounting for private sector liquidity which includes all flows of cash and credit as well as major central banks.

Liquidity (QE, GMI) guides markets. The NASDAQ-100 pulled back in 2022 and from July to October 2023 when global liquidity fell.

Era of QE

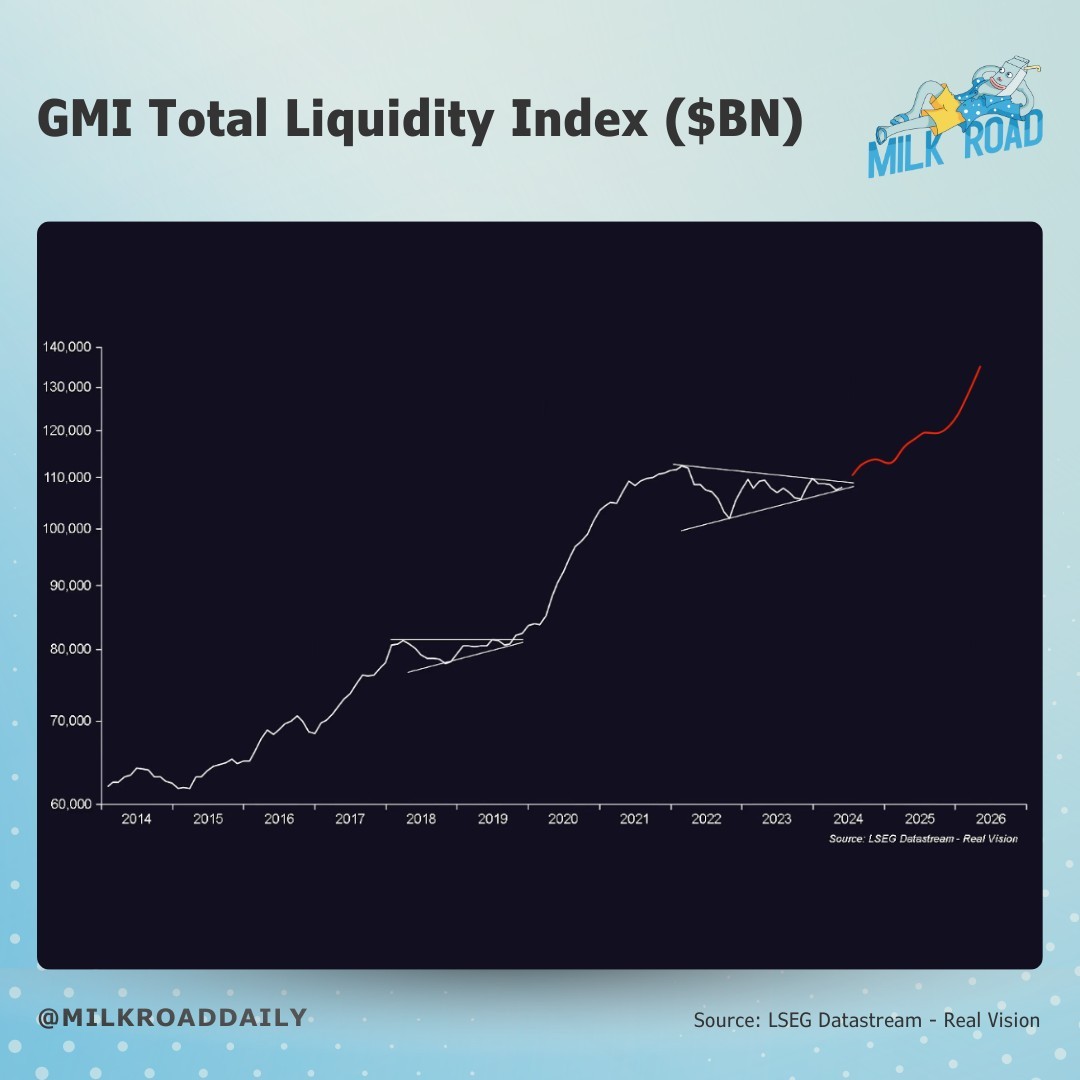

QE is just now reaccelerating. The recent global crash should further spur a wave of QE. QE had been decelerating starting in 2022 due to intense tightening as shown by the total liquidity index (Global Macro Investor's Global Liquidity Index). But major indices started into uptrends at the start of 2023 due to QE from China, QE from the Fed in March due to the banking disaster, and stealth QE where the US Fed prints fiat to pay for major expenses such as the massive debt interest which is now greater than its total annual defense spending, unfunded liabilities such as pensions and healthcare, uneconomic global warming laws, and the expanding war effort, among other key matters.

But after the long pause in total global liquidity, QE (GMI) is breaking out again. Every 100 days, the Fed must print about $1 trillion, but this amount is increasing since other factors continue to grow. Ray Dalio’s long term studies over the centuries shows fiat devaluation will now continue to accelerate since record levels of debt continue to accelerate due in part to onerous debt interest payments. This suggests much higher stock, bitcoin, and real estate prices in the years to come.

If we get further downside, watch the 200dma on the NASDAQ Composite for support then look for MAU&Rs (moving average undercut & rallies) and other U&Rs for potential long entries. If we get further upside, watch for names that have weak bounces into moving averages or price overhead that serve as resistance for potential short positions.