by Dr. Chris Kacher

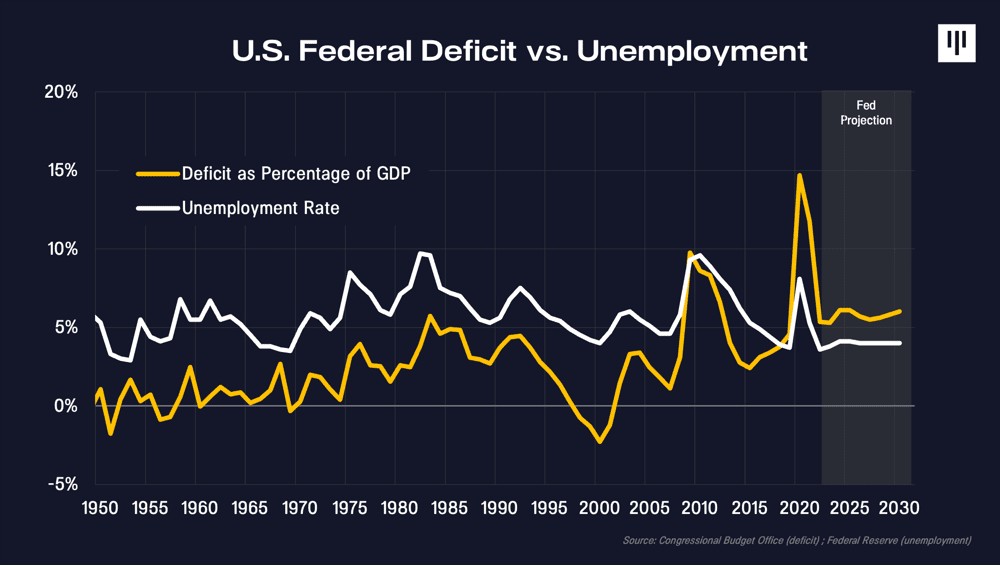

Populism, or the chasm between the haves and have-nots, is at levels not seen since the Great Depression of the 1930s. With record levels of debt, many metrics have shown unprecedented historical signals. For example, the budget deficit as a percentage of GDP used to be much lower than the unemployment rate. Just as important, it rose and fell with the economy and the rate of unemployment. Deficit as a % of GDP as shown by the white line is now consistently above the unemployment rate as shown by yellow line. This is unlikely to change as deficits continue to increase. The interest payments on the deficit in the US has exceeded US defense spending for the first time since World War II.

Krugman-endorsed policies are now disconnected with what has worked for more than a century. Krugman is a Keynesian because he wants bigger government. This opposes theories from economists such as Friedman, Mises, Hazlitt, Hayek, and Rothbard that have been proven to work in reality. Unfortunately, due to wrongheaded economic policies, we now have massive deficits in boom times even with record low unemployment. But this is what quantitative easing (QE) in all its forms via central banks and fractional reserve banking is all about. It creates the largest legalized Ponzi scheme in existence.

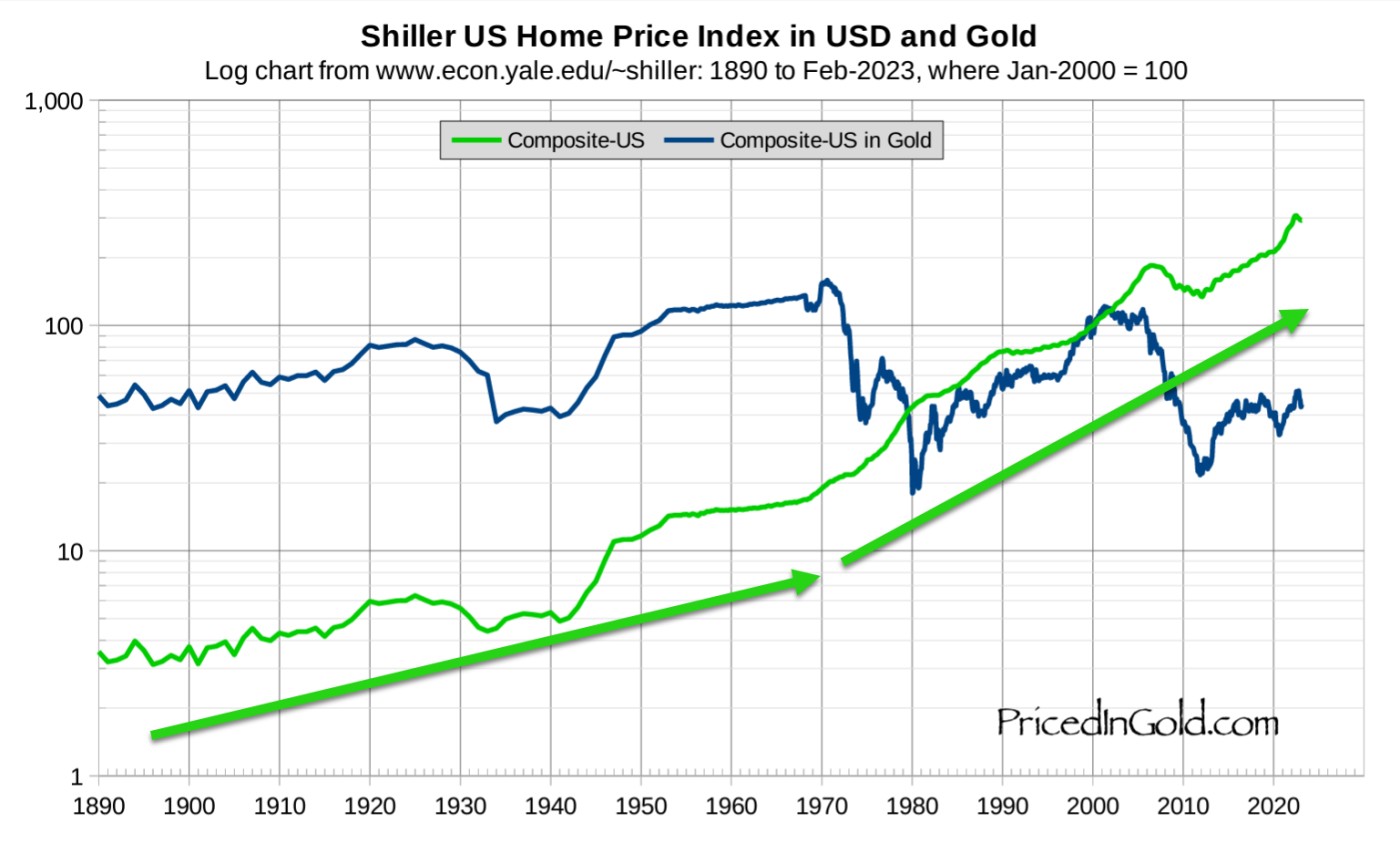

This inevitably destroys the middle class. The majority get pushed lower while only those in the top 10-15% who own assets such as stocks, bonds, and real estate benefit as fiat continues to sink. Older generations who are more likely to own property have often become millionaires due to the sheer price increases in real estate over the decades. About 1 in 8 families are now millionaires in the US. Real estate prices have historically risen exponentially since the year 1890. On an exponential plot, you can draw a straight line through the price increases which proves this observation. But the exponential trajectory markedly increases once Nixon took the dollar off the gold standard in 1971. This gave the Fed free reign to print as much as they needed.

In consequence, startling statistics over the last several years have only worsened. Figures such as 75% of Americans and British either live paycheck-to-paycheck or dont have $1000 in savings for emergencies make for a house of cards economy. The question is whether technologies such as AI and blockchain which provide exponential utility and value creation will be sufficient to raise the tide that lifts all boats to avert a major revolution or global war. In the meantime, even though the pace of inflation is slowing, remember that prices are still rising and tend to rise the most in areas we need the most such as education, healthcare, food, and energy. Reasons to create more money will surface such as a growing global conflict, servicing interest payments on the growing debt, and honoring unfunded liabilities such as pensions and IRAs. At present, with the Fed having signalled an end to rate hikes and the start of rate reductions, expect easy money times ahead. This means higher prices in stocks, bonds, Bitcoin, real estate, and other hard assets. The Dow Jones Industrials hit new all-time highs, the S&P 500 is a heartbeat away from all-time highs, and the NASDAQ is not far behind.

In consequence, startling statistics over the last several years have only worsened. Figures such as 75% of Americans and British either live paycheck-to-paycheck or dont have $1000 in savings for emergencies make for a house of cards economy. The question is whether technologies such as AI and blockchain which provide exponential utility and value creation will be sufficient to raise the tide that lifts all boats to avert a major revolution or global war. In the meantime, even though the pace of inflation is slowing, remember that prices are still rising and tend to rise the most in areas we need the most such as education, healthcare, food, and energy. Reasons to create more money will surface such as a growing global conflict, servicing interest payments on the growing debt, and honoring unfunded liabilities such as pensions and IRAs. At present, with the Fed having signalled an end to rate hikes and the start of rate reductions, expect easy money times ahead. This means higher prices in stocks, bonds, Bitcoin, real estate, and other hard assets. The Dow Jones Industrials hit new all-time highs, the S&P 500 is a heartbeat away from all-time highs, and the NASDAQ is not far behind.Dollar vs. Bitcoin

The chart shows that when the RSI (relative strength index) of DXY has dropped below 50, BTC has gone on a strong run. This has only happened twice since 2011 with the time in 2009 and 2010 not relevant since BTC was still embryonic, trading for a few pennies or fractions thereof. So while three times is statistically insignificant, all three times enjoyed dovish Fed policies. Data willing, we may be at the brink of such an opportunity. The trend is your friend until the end when it bends.

We should see continued weakness in the dollar as the Fed and other central banks look to lower rates sooner than later as the rate of inflation continues to fall. Figures released by the Office for National Statistics in the UK which showed that consumer price inflation slowed to 3.9% from 4.6% in October. This marked the lowest reading since September 2021 and was below analysts’ expectations of 4.4%. The ONS said the largest downward contributions came from transport, recreation and culture, and food and non-alcoholic beverages. Core inflation - which strips out volatile food and energy prices - fell to 5.1% vs. estimates of 5.6% in November.